Many Americans are now arriving at retirement age with an average of $60,000 in savings including their IRAs and their 401ks. That is not nearly enough to pay for a retirement that could easily last 20 or 30 years. And the Center for Retirement Research at Boston College finds that 43 percent of workers risk being unable to maintain their standard of living in retirement.

Many Americans are now arriving at retirement age with an average of $60,000 in savings including their IRAs and their 401ks. That is not nearly enough to pay for a retirement that could easily last 20 or 30 years. And the Center for Retirement Research at Boston College finds that 43 percent of workers risk being unable to maintain their standard of living in retirement.

The Employee Benefits Research Institute reports that more than 1/2 of workers age 45-54 have saved less than $50,000 for retirement. A recent Fidelity study found that the average boomer is on track to replace just 60% of his or her current income in retirement, even with help from Social Security and pensions.

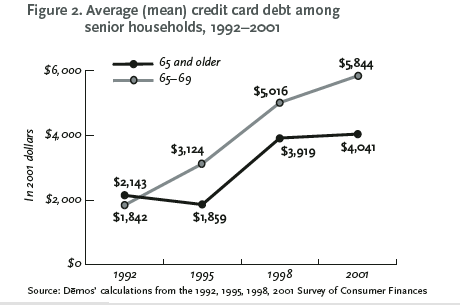

According to a 2003 study "Retiring In The Red", conducted by Demos, nearly one-third of senior citizens in the U.S. carry card balances. But within that group, the average debt is $4,041 — an 89% increase over the past decade. (For all age groups, the average increased by 53% over this same time period, according to Demos.) The debt increase is particularly sharp during the first years of retirement, the study found: People aged 65 to 69 saw their credit-card balances grow by 217%, to $5,844, during the decade. And since the data used in the study come directly from consumers, rather than creditors, the real numbers could be much higher.

The rate at which retirees are filing for bankruptcy has more than doubled over the past 10 years. Retirees are now the fastest-growing segment of bankrupted Americans, according to research by the Consumer Bankruptcy Project at Harvard University.

Credit-card debt used to be considered rare among the elderly, many of whom have spent most of their lives not owning a credit card, let alone carrying a balance that's beyond their means. But it is rare no longer.

"Credit-card debt is becoming common among older Americans in the same way it's common among all other age groups," says Tamara Draut, a director at Demos, a New York-based research and advocacy company, and co-author of "Retiring in the Red" study.

Among seniors (over 65) with incomes under $50,000 (70 percent of seniors), about one in five families with credit card debt is in debt hardship - spending over 40 percent of their income on debt payments, including mortgage debt.

And more are coming. As the transitioners (aged 55-64) are spending 31 percent of its income on debt payments, a 10 percentage point increase over the decade.

What's driving this trend? Longer life expectancies, soaring medical costs, and a bear market that blindsided many seniors. Survival Debt and the American Consumption Ethic have left little to invest for our future retirements. Expect to face more of this as we exit the age of the corporate pension and enter the age of the decline of Social Security assistance, or even inheritances. Of course, there is still the Lotto.

Tuesday, July 11, 2006

Trend: Bankrupt!: Retiring In The Red

Subscribe to:

Post Comments (Atom)

1 comment:

Great site lots of usefull infomation here.

»

Post a Comment