We've noted before about the exploding Payday Lending industry which reaped $10 billion in sales in 2000 to $40 billion, including $6 billion in interest rates and fees, in 2003.

We've noted before about the exploding Payday Lending industry which reaped $10 billion in sales in 2000 to $40 billion, including $6 billion in interest rates and fees, in 2003.

A Defense Department report issued last month found that as many as one in five (20%) U.S. service members “are being preyed on by loan centers set up near military bases,” which can charge annual interest rates of 400 percent or more. Increasingly, soldiers have debt levels so high they are barred from serving overseas; others suffer from “bankruptcies, divorces and ruined careers” due to the strain and stress of debt. The Pentagon has joined consumer, military, and veterans groups in backing a bipartisan amendment that places a cap of 36 percent on high interest rates for short-term payday loans to military members.

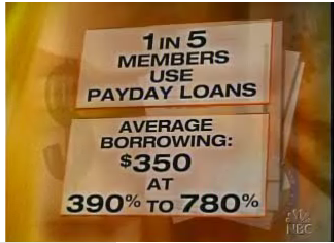

Payday lenders offer high-cost, short-term loans marketed as cash advances on the borrower’s next paycheck to cover an "emergency need." Lenders charge roughly $15 to $25 per $100 loan for two weeks, and most loans are extended for several weeks because the borrower is unable to pay back the original loan amount. The average loan "is $350 and has an annual interest rate of 390 percent to 780 percent," meaning the average borrower "pays back $834 for a $339 loan." Between 13 percent and 19 percent of U.S. servicemembers -- roughly 175,000 people -- took out such loans last year. "Because of the high-risk terms, borrowers often get caught in a vicious cycle of chronic debt. When they cannot afford to pay back the fees plus the principal at the end of the two week period, borrowers are forced to pay another high fee to roll over the loan for an additional two weeks or take out another loan to pay off the first loan, thereby getting trapped in a costly and often devastating cycle of 'back-to-back' loans." Payday lenders systematically target military families, who are an ideal demographic for payday lenders because they usually have a steady government paycheck with little to spare at an average of $1,200 a month for new recruits. A 2005 report found that in 19 of 20 states studied, payday lenders were "located in counties and ZIP codes adjacent to military bases in significantly greater numbers and densities than other areas."

Payday lenders systematically target military families, who are an ideal demographic for payday lenders because they usually have a steady government paycheck with little to spare at an average of $1,200 a month for new recruits. A 2005 report found that in 19 of 20 states studied, payday lenders were "located in counties and ZIP codes adjacent to military bases in significantly greater numbers and densities than other areas."

The Pentagon states that payday lending "undermines military readiness, harms the morale of troops and their families, and adds to the cost of fielding an all volunteer fighting force," problems already exacerbated by the war in Iraq. Debt can distract service members from their duties or cause them to become security risks open to compromise. The Navy and Marine Corps denied security clearance to about 2,000 service members nationwide last year because of concerns that their indebtedness could compromise key operations. The Pentagon report outlines current efforts to combat abusive practices through education and credit counseling for service members, but also acknowledges that education is only part of the solution. NBC's Martin Savidge reports .

NBC's Martin Savidge reports .

via Center for American Progress and MSNBC

Wednesday, September 27, 2006

Bankrupt!: Unbanked: Payday Lending to Military

Subscribe to:

Post Comments (Atom)

1 comment:

Learn The Secret Today

Find The secret to the secret at http://loans4bills.com/. If you want to find out how you can get american home loans direct refinance rates mortgage help visit us

Post a Comment